Cuts Both Ways

As the Fed is on the verge of embarking reducing the balance sheet i.e. Quantitative Tightening, the song by Gloria Estefan, the three time Grammy award winner and one of the first Latin artists to break into international markets, comes to mind. For most of the past decade-and-half, beginning in November 2008, there has been a QE program in action somewhere in the world. It has been a golden era for asset performance but the QE impact cuts both ways. The reversal will likely usher an era of challenges for portfolios constructed during the QE period.

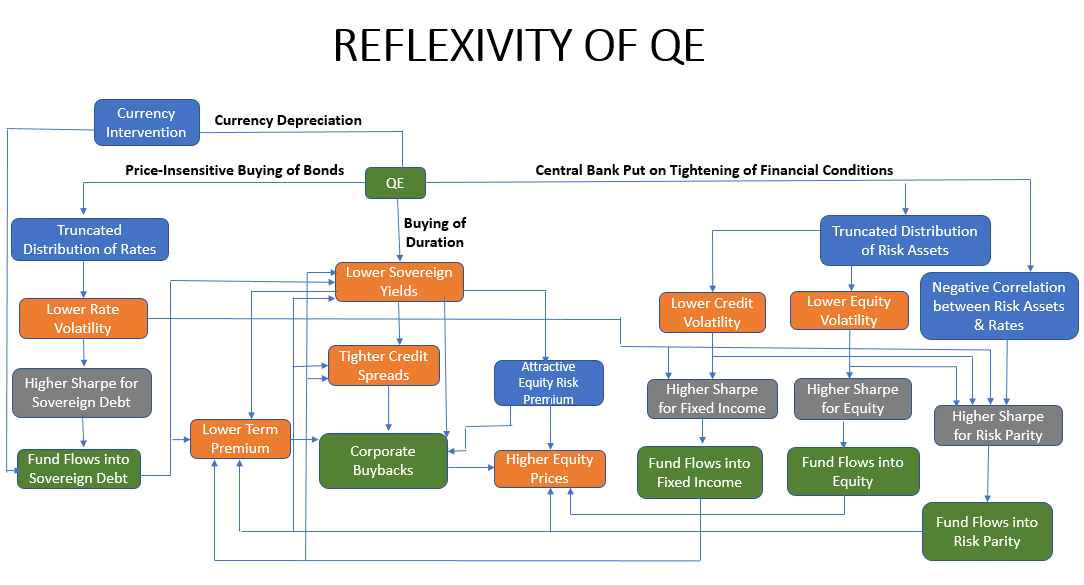

Lot has been written by central bankers, academics, economists and strategists around the world about the various channels through which Quantitative Easing impacts markets and the economy. I want to focus specifically on the Reflexivity aspect of QE ('Reflexivity' is a theory conceived and explained lucidly by George Soros in his book 'Alchemy of Finance'). I've attempted to identify the major channels through with QE impacts markets and the flow chart below illustrates how the interaction between various channels creates a flow of funds dynamic that propagates the reflexivity of QE.

Once QT kicks off, this process will begin to unwind. Markets are forward looking and some recent price action is in anticipation of it. But the impact of this is going to take a lot longer to be fully reflected in markets as it is a reversal of a regime that we have been in for more than a decade. The valid counter argument is that we did QT in 2017 and it did not result in a regime shift and it ended up being more than reversed in 2020.

However, I think this time around is different for a few reasons -

In 2017, balance sheet reduction was seen as a prudent but not a necessary part of the tightening process and hence was referred to as 'its watching paint dry'. This time around by the chairman's own admission is part of the tightening package and is intended to be a tool to tighten financial conditions.

The starting size of the balance sheet and the pace of reduction is significantly larger than last time around. The expected impact on markets and financial conditions should correspondingly be larger.

The Fed has created a stand-by repo facility to address any market dysfunction should it arise from the QT program. This makes it less likely that QT will end for any reason other than a decision to end monetary tightening cycle and given starting point on inflation the balance sheet reduction this time should be a lot larger in aggregate.

This time the Fed is in true inflation fighting mode with its credibility at stake. This opens the door to more aggressive use of the QT program - selling mortgage backed securities has been mentioned as a real possibility. If the inflation backdrop stays sticky, other creative ideas like 'reverse twist' or even sales of treasuries may be considered.

The hurdle for the Fed to pause and change course like it did in 2018 is extremely high and there is a sense of 'buyers remorse' on the large scale QE program that was implemented in response to the Covid shock. In future recessions, even if needed, QE is likely to be more measured and conservatively calibrated.

In conclusion, multiple QE programs around the world alongside a backdrop of low and stable inflation created a decade long reflexive environment that allowed out-sized risk-adjusted returns to be delivered on a consistent basis on passive beta strategies which created more inflows and buy-the-dip mindset perpetuating the reflexive cycle. The end of the QE era is going to create an environment with higher volatility across assets and active alpha strategies will likely have their day in the sun. One thing is for sure - if indeed the QE era is ending, systematic trading algorithms (or habits for the humans) that have been developed based on market patterns over the past decade will have to be reworked.