Newton's Laws of Central Banking

No one needs a reminder on fifth grade physics but at the risk of sounding redundant, Newton's three laws of motion are -

Law 1: A body remains at rest, or in motion at a constant speed in a straight line, unless acted upon by a force.

Law 2: When a body is acted upon by a force, the time rate of change of its momentum equals the force.

Law 3: If two bodies exert forces on each other, these forces have the same magnitude but opposite directions.

They have parallels in central banking (or perhaps I'm just yet another engineer with a physicists' complex). In either case -

Law 1: The default state is that of inertia for central banks

Law 2: Large economic or financial shocks lead to significant policy shifts in central banks proportional to size of the shock

Law 3: Central bank actions impact financial conditions which in turn have an impact on future central bank actions until a point of equilibrium when the respective impacts are equal and opposite

What do these laws tell me about the environment today?

The signaling impact of a shift in central bank policy has a larger impact via change in financial conditions than just the actual policy move. In this regard, central banks are likely to be locked into their current state until there is convincing evidence that inflation risks have receded meaningfully or risks of a recession have risen meaningfully. This will likely keep Fed in 50bp-a-meeting mode beyond July meeting since the hurdle to stepping down to 25bp - which would be a de facto easing of financial conditions - is unlikely to be met by then. For the ECB, 25bp a meeting (assuming that's what they start at) will be the default policy for all of this year at the very minimum. But, this also means that policy uncertainty is relatively lower than earlier in the year when central banks were playing catch up to the inflation data and were calibrating the frequency and size of policy move.

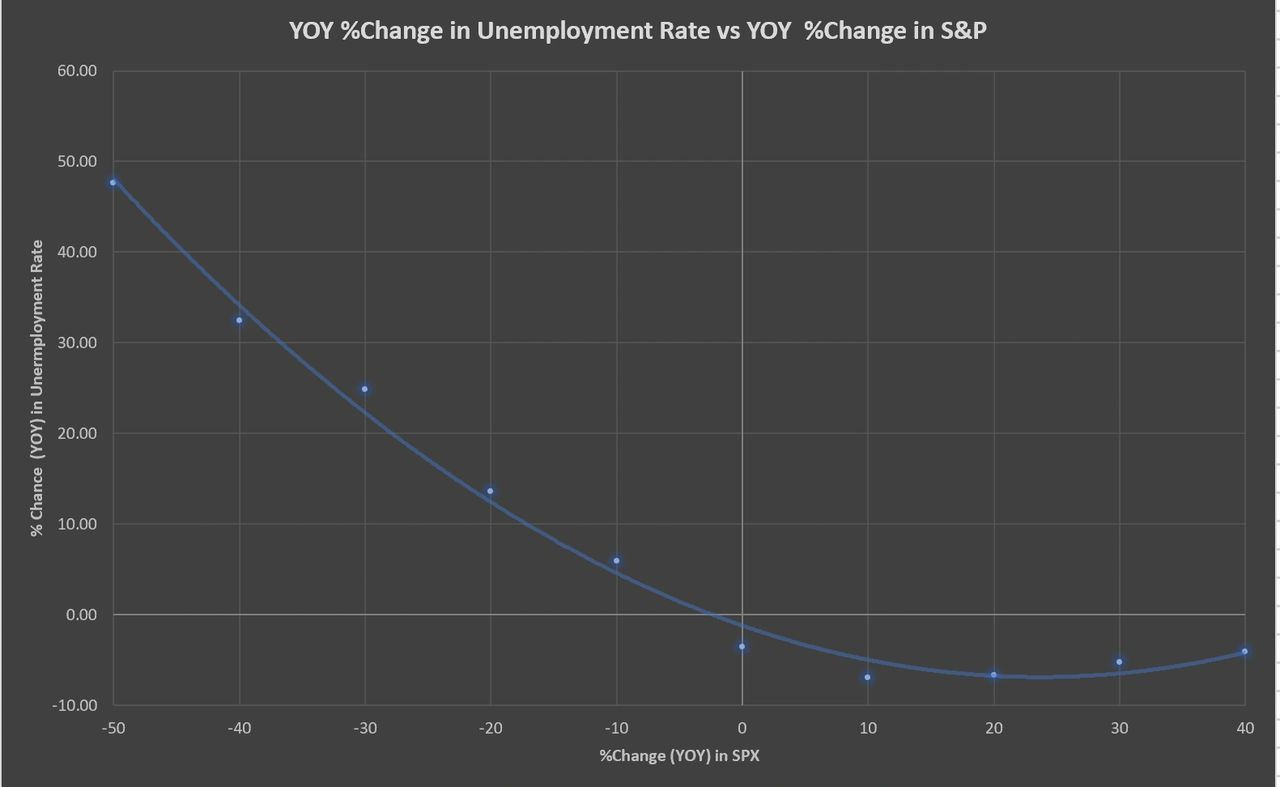

The idea of a 'wait-and-see' pause or a toning down of hawkish rhetoric once the Fed is closer to a neutral rate seems a bit of wishful thinking. The Fed is single-minded in its focus to convincingly demonstrate that it can indeed do what it takes to get inflation back down to its 2% target. The most likely reason that forces the Fed to reassess its path is a large financial shock via asset prices - but the hurdle for the Fed to respond is much higher that the last decade would suggest. An 70-year historical analysis of S&P returns versus Changes in Unemployment Rate (to be taken with a healthy grain of salt) would suggest that if we assume NAIRU is at least 10-20% above current UER of 3.6 (4 - 4.2%), it would need a decline in the vicinity of 20 - 30% in S&P to achieve that.

Finally, the stopping point for the Fed cannot be predicted ex-ante in isolation without knowing where financial conditions are and trying to do that is an exercise in futility. In my view, as inflation comes down but still remains above the 2% target, the Fed will move away from the idea that getting to its longer run neutral rate of 2.5% means that a pause is imminent. During the past normalization cycle, at Jackson Hole 2018, Powell gave a speech about framework of thinking about shifting stars during normalization* and Brainard followed it up with a speech on how to think about neutral rates**. I suspect, Jackson Hole and period following that will yield speeches that guide the market away from its last remaining part of forward guidance i.e. longer run neutral rate acting as an indication of stopping zone for the Fed.

In conclusion, Fed will likely stay on the path of 50bp longer than market currently believes and unless there is a large equity market correction (>25%) the combination of financial conditions and progress on inflation will determine terminal rate than some theoretical longer run neutral estimate. And just like once-a-quarter hiking cycle or 25bp hiking increment quickly became obsolete in this cycle, the 2.5% neutral rate will meet with the same fate.

* https://www.federalreserve.gov/newsevents/speech/powell20180824a.htm

** https://www.federalreserve.gov/newsevents/speech/brainard20180912a.htm