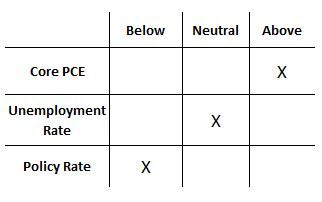

Tic Tac Toe

The Fed reaction function can be visualized by mapping the 3 variables - unemployment rate, core inflation and policy rate relative to their neutral levels on a Tic Tac Toe Grid.

Though I have characterized the unemployment rate as neutral, it can certainly be argued that at least on a short term basis it is below neutral. Taking inventory of where we are now -

Core Inflation

The durable goods economy is showing signs of consumer spending shifting away from goods to services. The pent-up demand for autos is yet to be fulfilled. But once that is achieved, what lies ahead is at least a couple of quarters if not more of a slowdown in goods economy with manufacturing PMI likely to dip below 50. It is reasonable to forecast that the goods inflation should slow as easing of supply chains, cooling demand for goods and higher inventory build will lead to lower prices. How fast and to what level will overall core inflation move towards is yet to be determined.

Unemployment Rate

Virtually every speech by Powell in 2022 has emphasized how tight and imbalanced the labor markets are on pretty much any metric. While the consumer spending shift towards services away from goods helps in relieving core goods inflationary pressures, it will likely make the problem worse for labor market. The services sector accounts for close to 85% of employment (and even excluding retail trade/ transportation/ warehousing it is 70%) and increase in spending on services is likely to keep the labor market tight in the very least if not make the imbalances worse.

Policy Rate

Consecutive 50bp hikes next couple of meetings for the Fed seem pretty much a fait accompli (pun intended). This puts the Fed in the vicinity of the lower end of its estimate of neutral rate. The hurdle set by Powell to see compelling evidence of slowdown in inflation and labor markets and his willingness to go above neutral if necessary makes it quite likely that Fed will continue hiking above neutral even if it steps down its pace to 25bp a meeting from its current 50bp a meeting pace.

Fast-forward to end of year 2022, it is a plausible scenario that the economy could be in what I characterize as a state of 'Triple 3' -

Core Inflation at 3%

Unemployment Rate at 3%

Fed Funds Rate at 3%

Of course, the likelihood that each of the three variables are exactly at 3% is low, but the relative direction of travel for each variable is not too far from the Fed's own forecast. The outlook for the Fed under this scenario gets a whole lot more interesting. On one hand, the progress in inflation would be notable and consistent with the expectation that goods inflation would reverse bringing core inflation closer to its target. On the other hand, it would give them little comfort to see that labor markets remain tight creating elevated risks of inflation failing to fall closer to their 2% target and inflation expectations moving higher. With policy rate at levels already above neutral, Fed would want to maintain its hawkish stance but with less urgency. My bias would be that the Fed would continue to hike at a 'measured pace' i.e. 25bp a meeting until it receives convincing evidence that either the labor market is reversing or that inflation is slowing to levels consistent with its 2% target. The market would have to prepare for a more prolonged cycle than what is currently priced.

The evidence increasingly points to short-run NAIRU being quite a bit higher (>4%) than Fed's own long-run estimate. Looking ahead, a scenario in which labor market does not cool sufficiently unless policy is significantly tighter than its neutral estimate or one in which a deteriorating labor market fails to cool inflationary pressures decisively are both bad outcomes for the Fed. How this Fed cycle evolves in reference to these two outcomes has important implications for mapping the Fed. The former would imply that policy rates would need to be hiked to and maintained for longer at levels well above neutral and the latter implies the Fed cannot be pro-active and as aggressive in responding to downside risks to the economy. The risks of hard landing of the economy and deeper risk asset declines are high in both these outcomes.

Great article.. I think if you get the Triple 3, it'll be a homerun scenario for Fed and economy. 3% nominal rate with 3% core inflation is still lower bound of 'real' neutral rate of 0%. Also, a 3% core inflation rate is in the vicinity of 'opportunistic disinflation' territory. if that scenario materializes, i think Fed will continue to run down the balance sheet and perhaps hike to 3.5% (i.e. 2x25bps ) in a leisurely fashion and stop. Equities may not have any real issues except for margins, but that's a wholly endogenous issue for corporations.

However, getting 3% UE rate with 3% core is probably an unstable equilibrium, given current starting points. Even if that situation comes to fruition as a likely juxtaposition of deflating core goods vs services inflation, it may most likely be temporary. More likely is that wage pressures will be sufficiently large and persistent at 3% UE to keep pushing inflation higher again. in which case, they may have to keep hiking till UE rate is NAIRU bound or higher.

In any case, the Fed cannot respond to any downside risks till they get inflation to sub 2.5% or so. And it seems there is no path for inflation to come to reasonable territory without UE rate going up. It would be a miracle if risk assets escape a trip to the left tail!

Crafty! Love it